How Japanese Fuel-Economy Subsidies Affected Cars Sold in America

Multinational firms often sell nearly identical products across global markets. This raises the question of what happens when a government regulates a product in one country: Does that change propagate to the same product sold elsewhere? In Global Policy Spillovers: How Environmental Policies Propagate Through Product Attributes (NBER Working Paper 35197), Koichiro Ito, James M. Sallee, and Jonathan (Andrew) Smith study “attribute propagation”—the mechanism by which a domestic policy induces broader changes in product attributes through multinational firms’ product design decisions. The researchers focus on a Japanese fuel-economy subsidy introduced in 2009, which provided consumers purchasing vehicles above a weight-based fuel economy target with subsidies ranging from approximately $700 to $1,500—roughly 5 to 10 percent of the average price of a new car. Because Japanese automakers sold many of the same car models in both Japan and the US, some US-market vehicles were potentially exposed to the subsidy’s influence while others—Japanese-brand models sold exclusively in the American market—were not.

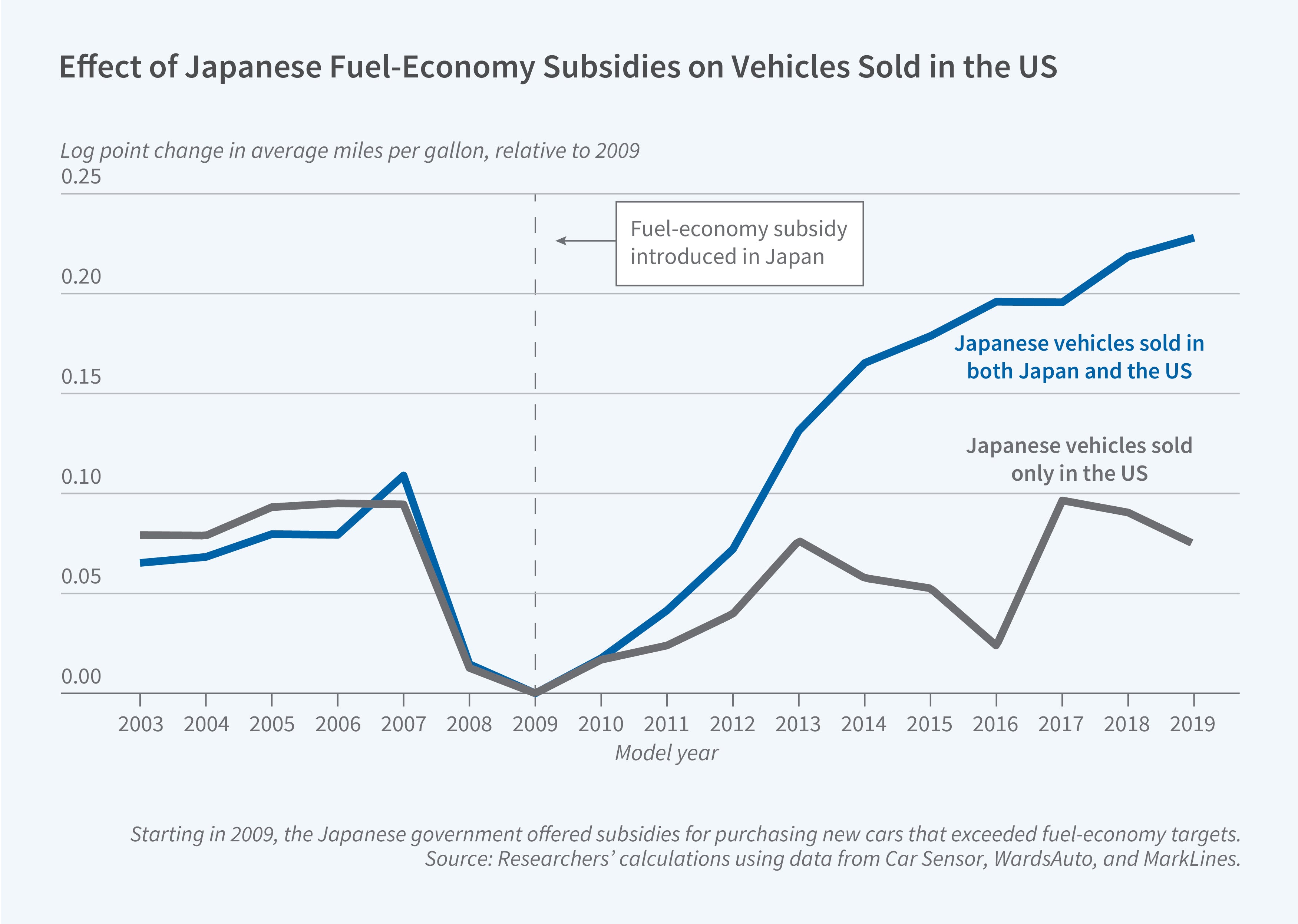

Japan’s 2009 fuel-economy subsidy improved the fuel efficiency of Japanese-brand vehicles sold in both Japan and the United States.

The researchers compare fuel economy trends between these two groups of vehicles over the 2003–2019 period, drawing on vehicle specification records from Car Sensor (Japan) and WardsAuto (US) as well as monthly model-level sales figures and production data from MarkLines. They find that for vehicles sold in both Japan and the US, the subsidy generated an 8.7 percent improvement in US fuel economy relative to vehicles sold by Japanese automakers exclusively in the US. They estimate that the direct effect in Japan was larger: a 25.2 percent improvement. They also find that US automakers, whose sales volumes in Japan were too small to make compliance with the subsidy worthwhile, showed no statistically significant change in the fuel economy of their US vehicles.

The researchers find a greater degree of attribute propagation when a given vehicle is produced in a single facility and shipped to multiple markets, and on models with smaller preexisting fuel economy differences between the Japanese and US markets. The latter finding suggests that less-differentiated products are more likely to be jointly designed for multiple markets.

The researchers estimate that global CO2 reductions as a result of the Japanese policy were 5.4 times the reductions associated with vehicles sold in the Japanese market. This is because the US vehicle market is substantially larger than the Japanese market, and because American drivers travel approximately 11,218 miles per vehicle annually compared to 3,206 in Japan.