The Rise of $500 Million Bond Offerings by Emerging-Market Firms

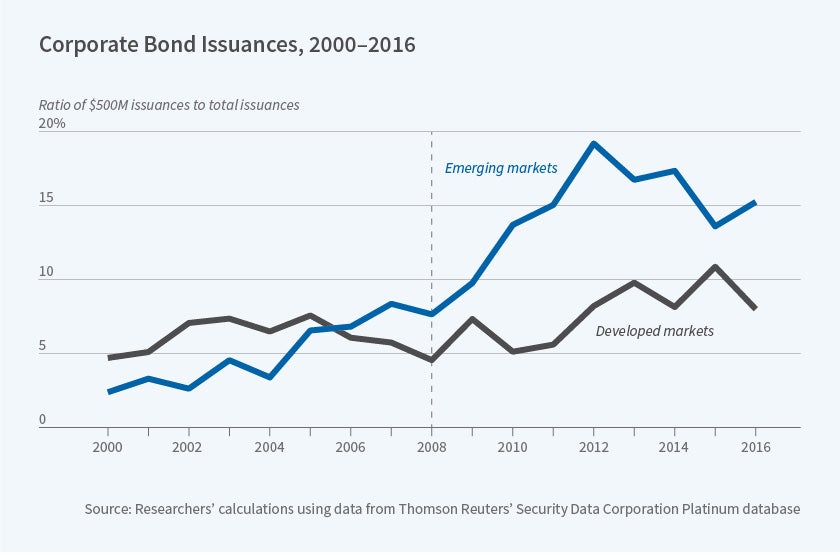

Between 2000 and 2008, bond offerings of at least $500 million represented a third of the total debt issued by private-sector emerging-market firms. After 2008, that share nearly doubled.

After the global financial crisis of 2008, there was a surge in debt issued by emerging-market companies and a sharp uptick in the size of the bond offerings from these firms. Larger bond offerings, in particular those valued at $500 million or more, are associated with lower interest rates, so the attraction for borrowers is clear. But why were bond market investors so attracted to these large issues?

Charles W. Calomiris, Mauricio Larrain, Sergio L. Schmukler, and Tomas Williams, in a new study entitled Search for Yield in Large International Corporate Bonds: Investor Behavior and Firm Responses (NBER Working Paper No. 25979), argue that a search for yield by institutional investors following the 2008 crisis is a key component of the explanation. While these investors were prepared to accept the greater risk associated with the debt of emerging-market companies in return for the higher yield that it offered, they targeted their bond purchases to large debt issues included in a key financial market index. This translated into a significantly lower interest rate for these large debt issues. As evidence for this hypothesis, the researchers point out that these patterns are not apparent in the issuance of investment- grade bonds by firms in developed economies.

The researchers show that the financial crisis ushered in a shift in the structure of private-sector emerging-market debt. They examine nearly 20,000 debt issues from 4,965 firms in 68 countries between 2000 and 2016, and find that the yield on newly issued debt fell sharply for emerging-market bond issues of $500 million or more after 2008. The decline was far more pronounced than that associated with smaller bond issues from companies in emerging markets, or than that for large bond issues by investment grade corporations in developed nations. This decline in yields coincided with an increase in the issuance of these bonds. Before the financial crisis, bond issues of $500 million or more represented a third of the total debt issued by emerging-market companies. After 2008, they represented 62 percent of new debt issues, and 18 percent of all bond issuances had a face value of exactly $500 million.

To explain the significance of the $500 million threshold, the researchers note that a key index for emerging-market corporate bonds, the J. P. Morgan CEMBI Narrow Diversified Index, only includes issues that are valued at $500 million or greater. When the financial crisis ushered in a period of low interest rates, many large institutional investors, looking for higher yields, began to buy up corporate debt in emerging markets. These new or "cross-over" investors, many of them unfamiliar with the market, tended to buy debt that was included in market indexes because the debt was more liquid than other emerging-market corporate debt and thus easier to sell, if needed. Cross-over investors tended to buy more large-denomination bonds than funds that specialized in emerging-market corporate debt. Furthermore, new emerging-market specialist funds, eager to attract investors interested in the emerging-market corporate asset class, sought to hold debts that were included in the index to reduce the risk that they would diverge from the index.

The rise in demand for the $500 million bonds in turn lowered the financing costs of issuing such bonds by roughly 100 basis points — what the researchers call a "size yield discount." That discount made issuing such bonds attractive not only to the largest firms, whose investment plans might require such large debt issues, but also to moderate-size firms that might stretch to issue such a bond because of the lower financing cost, and then hold part of the debt proceeds in cash until future investment opportunities emerged.

— Laurent Belsie