The Financial Impact of Cognitive Decline Before Dementia Diagnosis

Dementia imposes substantial costs on individuals and society through healthcare expenses and caregiving needs. However, the economic consequences may begin years before clinical diagnosis, as cognitive decline can impair financial decision-making, compromise portfolio management, and increase susceptibility to fraud. In Dementia and Long-Run Trajectories in Household Finances (NBER Working Paper 34659), Jing Li, Kathleen M. McGarry, Lauren Hersch Nicholas, and Jonathan S. Skinner use nearly two decades of data from the Health and Retirement Study (HRS) to compare the financial trajectories of individuals who eventually develop dementia with those of similar individuals who do not.

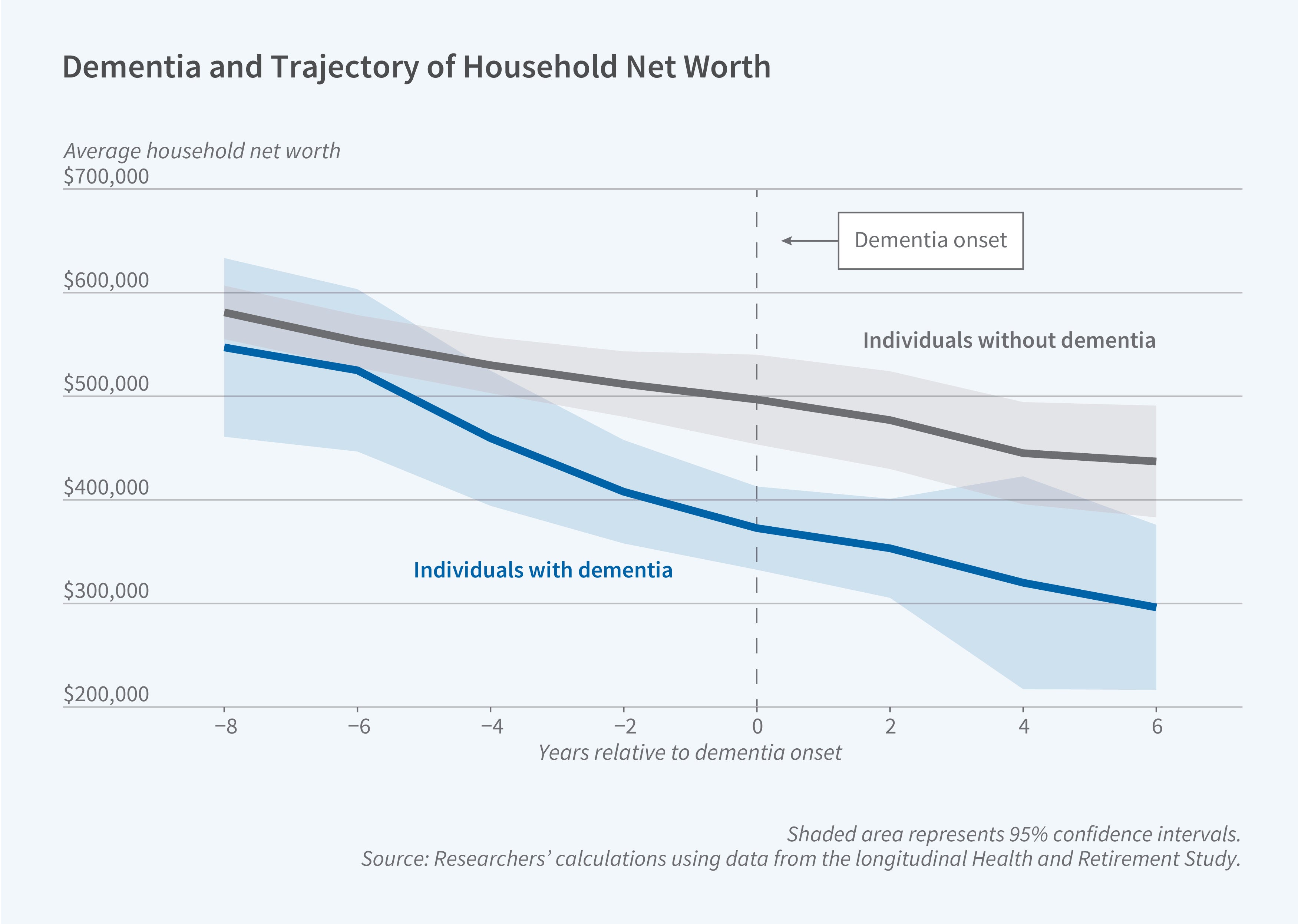

Household wealth begins declining approximately six years before dementia onset, primarily through impaired management of liquid financial assets.

The researchers classify individuals as having dementia when their predicted dementia probability exceeds 50 percent, capturing cognitive impairment regardless of clinical diagnosis timing. The study includes 2,312 individuals who are classified as having dementia, and 8,431 controls who are not so classified. The sample households are observed between 2000 and 2016.

The researchers estimate that wealth divergence between those who develop dementia and those who do not begins approximately six years before dementia onset. The gap in mean household net worth between the two groups widens roughly fourfold during this period, from about $30,000 before divergence to nearly $125,000 at dementia onset, with financial wealth and non-financial wealth accounting for roughly two-thirds and one-third of the gap, respectively. The relative decline in financial wealth is most pronounced between six and four years before onset, while the relative decline in non-financial wealth accelerates closer to onset.

Neither reduced earnings nor higher healthcare spending can explain the magnitude of the wealth gap. The differential earnings decline at dementia onset is less than $1,000. Out-of-pocket healthcare spending among those with dementia exceeds that of controls by about $1,000 to $1,600 per year in the years before onset, far too small to explain the wealth decline. The study finds no evidence of increased total household spending before dementia onset, contradicting explanations based on intentional "spend-down" to qualify for Medicaid nursing home coverage. Respondents show no awareness of an elevated risk of needing long-term nursing home care even though the likelihood of residing in a nursing home is 17 percentage points higher at onset for those with dementia than for the control sample.

The researchers conclude that impaired financial decision-making is the most likely source of the diverging financial trajectories between those with and without dementia. The largest wealth declines occur in liquid assets requiring active management, particularly stocks, bonds, mutual funds, and investment accounts, while checking and savings accounts show smaller but meaningful relative declines. In contrast, more restrictive retirement accounts show no relative change, likely reflecting the fact that accounts requiring less active management are more insulated from the effects of cognitive decline.

Individuals receiving timely memory-related diagnoses experience some wealth recovery after onset, particularly in financial assets, while those with late or no diagnosis continue losing wealth. Importantly, individuals with other serious medical conditions like cancer or heart disease show no similar pre-onset wealth declines, suggesting these patterns are specific to cognitive impairment.

The researchers acknowledge support from the National Institute on Aging of the National Institutes of Health grants K01AG066946 and R01AG069922.